"Money is made in

Tape Reading by anticipating what is coming

-- not by waiting till it happens and going with the crowd."

— Richard D Wyckoff

1. Introduction

"Tape Reading" is a classical method that uses to calculate the number of shares Accumulated or Distributed in a particular stock. It been used as one of the key tool to measure the "Internal Factor" by the Gurus, such as Jessie Livermore, Richard Wyckoff, etc... combined with other "Technical Factors" of the stocks/market.

The Proposition of how Tape Reading works is that The direction of the long term trends depends upon the amount of stock owned by and disposition of the insiders and key investors against the public. As Tape Reading can be use to deduce the Accumulation and Distribution activities, and even estimate the total percentage of shares in the insiders and key investors. Therefore it can use to deduce the price direction and level.

Those who are interested in the original detail of how to do so can find out from some old classic book, such as "Reminiscences of a Stock Operator -by Edwin Lefèvre" or "Day Trading Bible - Richard Wyckoff", etc.

2. How does Tape Reading Methodology been Evolved... Volume Based Indicators

While the "Tape Reading" methodology has be evolved over time and use in current charting indicators, it basic Proposition for the idea are the same:

A) The manipulators/ insiders must accumulate enough percentage of the shares in a particular stock before they would mark up the price for distribution.

B) The manipulators/insiders are having more information than the public, and would act before the public has notice the potential of the movement.

The direct translation of the methodology into the current charting indicator is the On Balance Volume(OBV).

The OBV calculation is basically adding the day's volume to a running cumulative total when the security's price closes up, and subtracts the volume when it closes down.

There are many other variations, such as volume weighted moving average etc... All are based on the same idea that volume should move first (or to be more exact, that the accumulation or distribution should start first), before the price would move strongly.

3. How and why does it loss it effectiveness

For those who are seriously want to find out how effective of those volume based indicators, it can check it out by doing a throughout back-test of data since the indicators inception till current date.(Which would not likely possible for individual to do so). Or to check out the results in some books. "The Encyclopedia of Technical Market Indicators, by Robert Colby" is one of a good book for doing so. (Some example backtest result -> Link)

It can be seen that all these volume-based indicators were performing wonderfully well from 60's,70's and all of a sudden, in the 80's, they lost their effectiveness as an indicator for buy and sell.

This is because there are more and more trading software available together with the Personal Computers, and computerized trading system for the big institution.

Let me explain...

For those volume based indicator that the public is using, they are mainly using the daily time-frame. So, the volume based indicator has made an assumption that the trading volumes are equally distributed in the whole day.

For the manipulators who would want to paint a picture of Accumulation, they can simple sell (distribute) the shares heavily, and just before the market is closing, they can suddenly buy back a couple of percent of what they had sold and push the price above yesterday's closing price. By doing so, all the Volume-based indicators will give false information.

One can simple do an experiment to proof this...

By collecting the one minute OBV, 15 minutes OBV, 60 minutes OBV and Daily OBV over a period of some time, say for two months. It would notice that there will be contradiction in the signals by the same indicators itself with different time frame.

In general, the shorter the time frame, the more accurate it would be. But then the problem would be that most softwares are not able to handle years of 1 minutes data (Unless the user has to write special peace of code to compress the 1 minutes OBV and load it back to match with the daily price chart.)

4. How to correct these errors and bring back it accuracy

Even so, that is to reduce the time frame down to a minute or second, there is still a problem with the accuracy in such volume based indicator. As there is one more factor that need to be consider...

As today, the market is full of trading news in all sort of controlled media...

So, when the manipulators wanted to purchase some particular shares, bad news would have came out to the public first, so that they can buy all the way down.

For the classical method, all fall in price during the transaction are considered as a distribution, while all raise in the price are considered as a accumulation. And, in the Figure 4, it shows a snap shot of the Raw data of a typical transaction. Since the Bid and Ask are very dynamic, and for some high volume stocks, it can be transacted a couple or few tens of time within a second.

So, the correct way to calculate the accumulated/distributed volume MUST take consideration of the Bid and Ask on the transacted price.

If the price is taken place on the Ask, it is a accumulation, and if the price is taken place on the Bid, it is a distribution.

When one can collect the data as such for a particular share, then... over a long period of time... he can then decode the INTERNAL CONDITION of the stock. And, it must use together with others Technical Analysis Tool to get a better timing.

For those who can understand this, it need no further explanation. So be it.

Bless You.

KH Tang

...BTW, The last chart show how the money was hidden in the stock... The manipulator are the one with deep enough pocket to go through the crash, and know exactly which one to accumulate...

-------------------------------------- Added on 10 July 2015 ----------------------------------------

Application of tape reading with modern software...

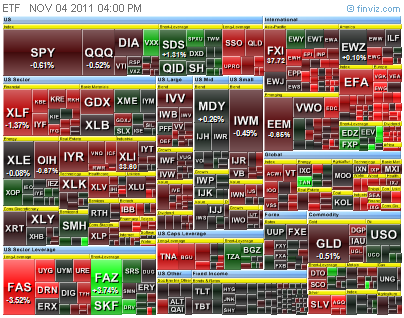

The last chart in this article - Wyckoff Schematic and Application shows the "Internal Condition" of a stock under the pool operation...

-------------------------------------------------------------------------------------------------------------

Relevant Articles:

-> Jesse Livermore's Secret Market Key <-

-> More articles on Stock Market Tools...<-

->Personal Finance<-

->Project Freedom<-

-> More articles on Stock Market Tools...<-

->Personal Finance<-

->Project Freedom<-

.jpg)

.jpg)

6 Comments->:

I had received a couples of similar questions on this article, and just to answer it here...

--------------------8<-------------------------

Hello,

I was just reading your blog and I can't seem to post any messages.

Anyway, you have a nice blog and great charts on the market. I am new to financial markets and I am trying to learn as much as I can. So I have two questions from your blog.

I really like the charts you've posted and want to know what kind of software you're using to study the market.

Second, from your post "Stock Market Tools (5) - Tape Reading", you have an indicator called "Volume Tape Reader". How is this indicator constructed? If it's proprietary indicator and you can't say, then I understand.

-Rick Chun

--------------------8<------------------------

I) The message can be post in two ways. One way is to click on the title of the article, and scroll to the bottom. Another way is to click on the number in the comment(0)<-, and it will bring you to the comment.

II) I had used many trading software since the first day of trading. My current favorite software is Amibroker and it is very customizable to any idea that you have, even to do low-level-graphic programming! Of course, one need to spend the time and effort to learn.

III) The objective for blogging here is to share ideas that I learned. Therefore, anything put up here is Not Proprietary. But, on the other hand, I do not give fish... If someone follow through the article in sequence, he/she should be able to programmed the system. Anyway, it would need a real-time data feed to get this Tape Reading data down to the real-tick level with buy queue,sell queue, and actual transaction price. It depends on which data supplier, some do have after hour download of the data, some don't. Some do compile the data and some don't. You need to find that out. Than you need to write an additional software to extract and compile into daily data, and then import in to your trading platform, and write some code to display it.

Bless You

KH Tang

It’s been a while I know but I just came across your post.

I was trying to code the indicator as suggested. My question is:

I can make out 3 different groups of data

a) Trade volume @ BID (12,726,497)

b) Trade volume @ ASK (12,414,354)

c) Trade volume all trades (25,853,521)

In this example I would have a distribution (A-D = -312,143)?

How do you handle the trades between BID and ASK (Total volume – (BID + ASK) = 712.670)?

Thanks for the ideas,

Tom

Good evening, Tom

Yes.

1) In your example, people are more proactive in selling that particular share by accepting a lower price (traded @BID). Therefore, it was a distribution of 312,143 shares.

2) In actual case, especially when the spread between the BID and ASK has a gap, that is more than one cent, say 10cents apart. Then, the transaction price could be happened anywhere in between and not exactly happen on the BID and ASK. I had workout a simple weightage formula to handle these transaction.

Say for the 10 cents gap example, if it was transacted at the middle, take is as netural (A = D). If it was taken place at 9 cents closer to the ASK => ACCUMULATION = Volume*( ASK*(9/10) - BID*(1/10)). DISTRIBUTION = TOTAL - ACCUMULATION.

So, if it was transacted at the middle point => 0 for both A & D.

Wish that you got the idea.

Bless You

KH Tang

if it was transacted at the middle, take is as netural (A = D).

Good day, Tom

Yes.

In your given example, you have got the first and major part of the work done. A-D = -312,143 (-ve => distribution).

The second portion of the work is to work out those transaction that is taken place in between BID and ASK.

Let me explain...

Lot of time, there will be Gap between the BID and ASK, that the difference is more than 1 cent. Take for example that there is a gap of 10 cents.

I would recommend you workout a weightage formula to handle such case.

=> ACC = Volume*( (Transacted Price - BID)/GAP);

=> DIS = Volume - ACC;

Where GAP = ASK - BID;

If the price is transacted exactly at the middle, you have ACC = DIS.

In fact, this formula work for all cases regardless of whether the transacted price fall onto BID or ASK or in anywhere in between.

Wish you figure that out.

Bless You

KH Tang

Great article KH Tang! We utilize tape reading strategies in our live trading room at www.TheDayTradingRoom.com. We also offer a great tape reading course www.TheDayTradingRoom.com/trade-setups-and-strategies-program-3/

Kh Tang'S Blog: Stock Market Tools (5) - Tape Reading >>>>> Download Now

>>>>> Download Full

Kh Tang'S Blog: Stock Market Tools (5) - Tape Reading >>>>> Download LINK

>>>>> Download Now

Kh Tang'S Blog: Stock Market Tools (5) - Tape Reading >>>>> Download Full

>>>>> Download LINK

Post a Comment